Dirty Business - What the Data Confirms

When Channel 4’s Dirty Business aired, it unsettled viewers not because it showed polluted rivers, but because it showed something more fragile: confidence draining from an institution in real time.

Executives insist the framework is sound. Regulators probe deeper. Public anger rises.

The crisis is not just environmental. It is systemic.

Three years of Legacy ESG trend data suggest that this collapse did not belong only to television. It unfolded — measurably — beginning in mid-2024.

And the turning point can be dated.

July 2024: When the Line Bends

On 10 July 2024, The Guardian reported that Thames Water had failed to complete 108 sewage treatment upgrades despite having funding allocated. It was not simply a pollution story. It was a delivery and oversight story.

Within weeks, regulatory scrutiny intensified. By May 2025, record enforcement penalties were reported nationally.

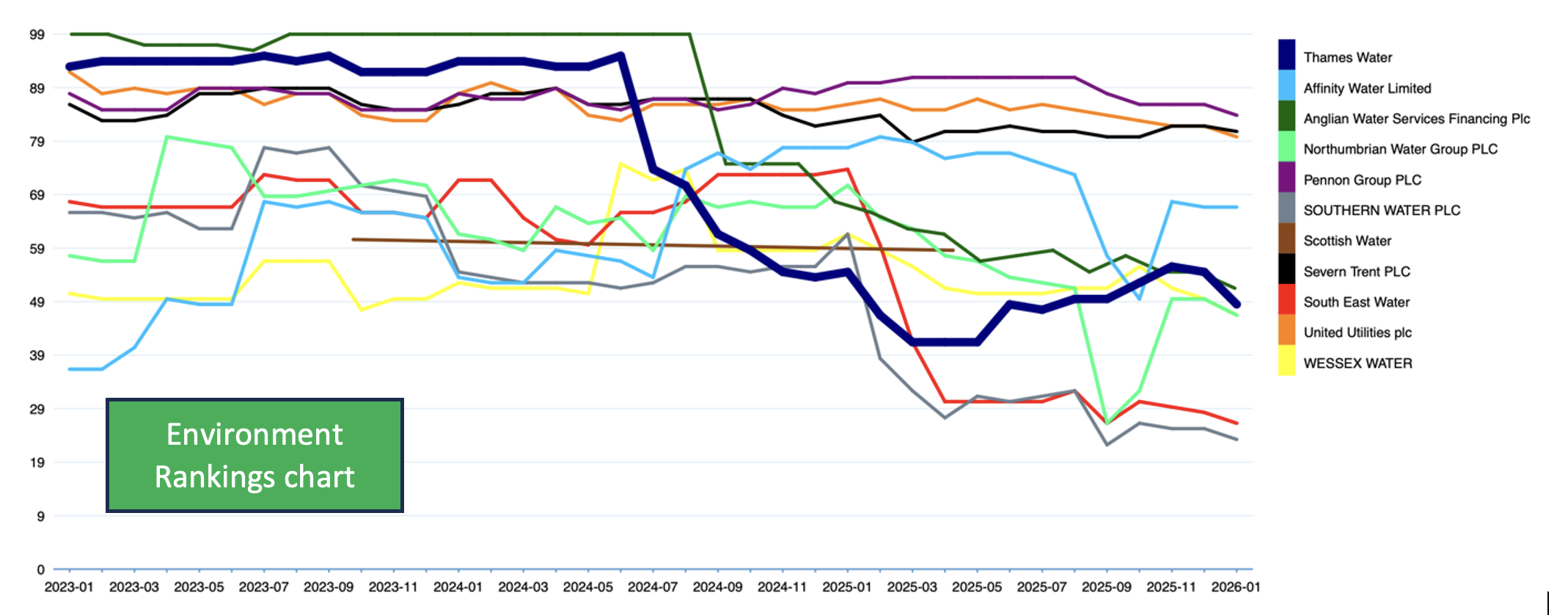

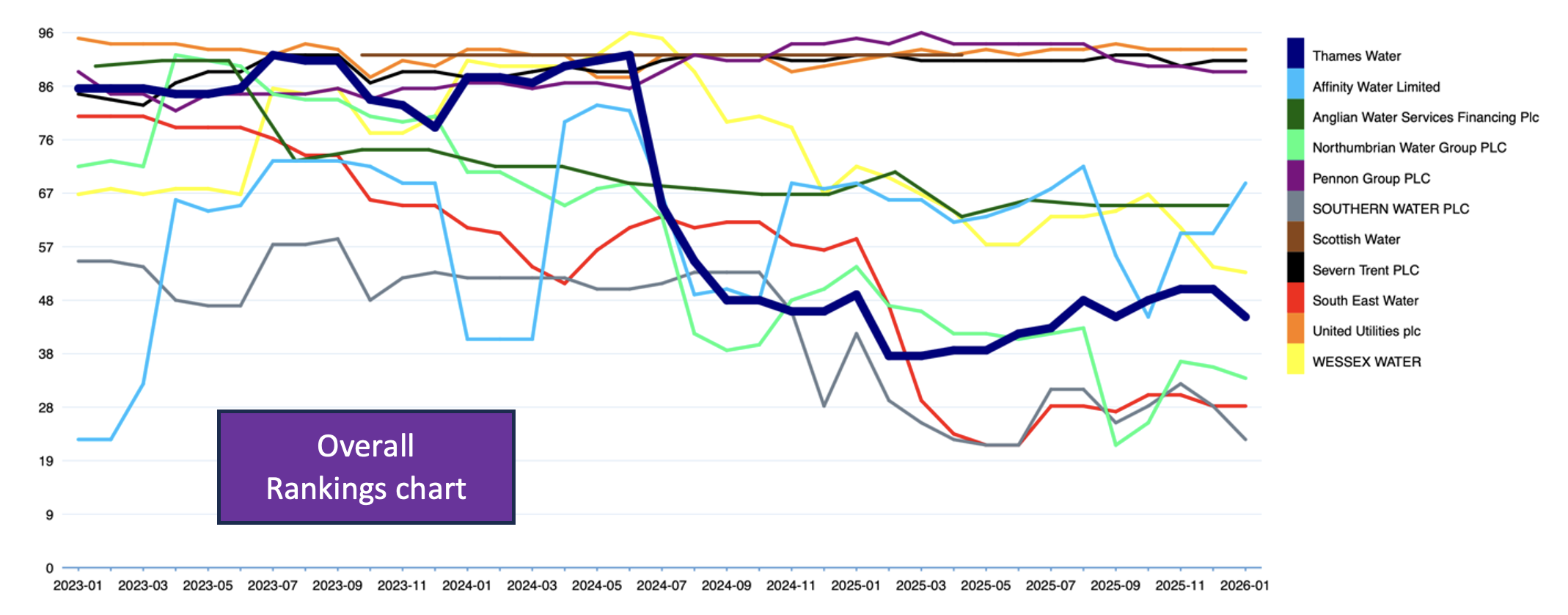

Now look at this Environment Rankings chart:

Until July 2024, Thames sat in the upper percentiles — high 80s and low 90s relative to peers. After July 2024, the line drops sharply. By early 2025, it stabilises in the 40s.

Environmental credibility did not erode gradually. It broke.

The System at the Centre: Operator Self-Monitoring

In Dirty Business, one of the most revealing scenes is not dramatic. It is procedural.

In a meeting, operator self-monitoring is described as reform. Water companies will monitor their own discharge activity. They will record their own environmental performance. They will notify regulators of breaches.

As Sophie Harrison of the Environment Agency explains:

“We want to strip out as much unnecessary regulation as possible… under operator self-monitoring, we’re going to be asking the water companies to monitor their own environmental performance, flagging any breaches to us as a priority.”

The language is administrative. The implications are structural.

Operator self-monitoring is built on a simple premise: that the entity generating the data can also be trusted to report it accurately. It shifts the regulator from constant inspector to supervisory auditor. It reduces friction. It assumes alignment.

When credibility holds, it is efficient.

But the system has no buffer against doubt. Its legitimacy depends entirely on confidence in the operator.

When environmental performance begins to be questioned publicly, the issue does not remain confined to spills or discharge volumes. It migrates.

Was monitoring sufficiently robust?

Was reporting complete?

Was oversight proportionate?

In July 2024, environmental confidence in Thames Water drops sharply. The ESG indicators register it. Media scrutiny accelerates. Political attention follows. Within months, governance confidence begins to deteriorate as well.

The sequence is not random.

Environmental doubt precedes governance doubt because environmental reporting is where trust is first tested. If the environmental numbers are uncertain, every subsequent assurance becomes fragile.

Operator self-monitoring works only while the data is believed. Once belief weakens, each reported metric carries a second meaning: not just performance, but credibility.

The data does not dramatise this shift. It records it.

Mid-2024 is where the inflection becomes measurable.

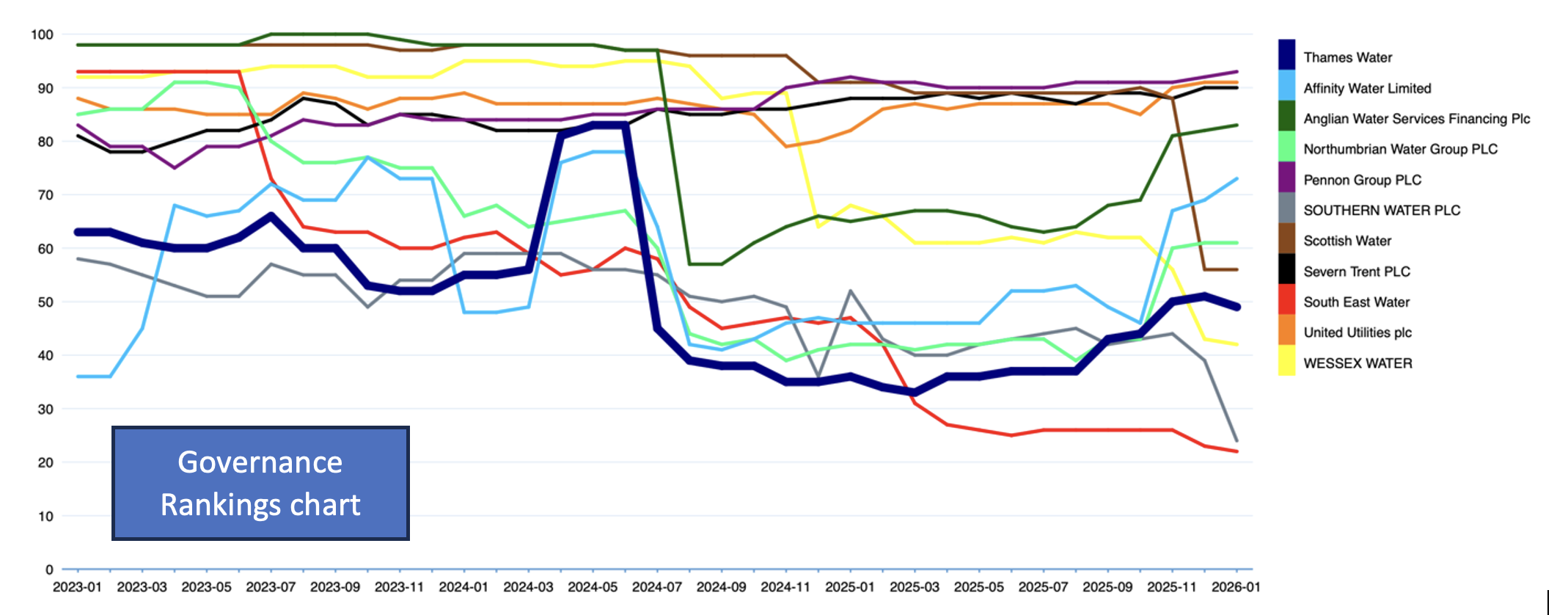

Governance: When Oversight Fails

Through early 2024, Thames’s governance percentile hovered in the low 60s. After mid-2024, it plunged into the 30s.

Governance percentiles reflect perceived board effectiveness, transparency, leadership ethics and structural oversight.

The decline coincided with sustained reporting — much of it led by The Guardian — on enforcement packages, oversight concerns and financial governance.

In Dirty Business, this is the boardroom turning point. Structures still exist, but belief in them fades.

Once governance credibility collapses, recovery becomes harder than repairing pipes.

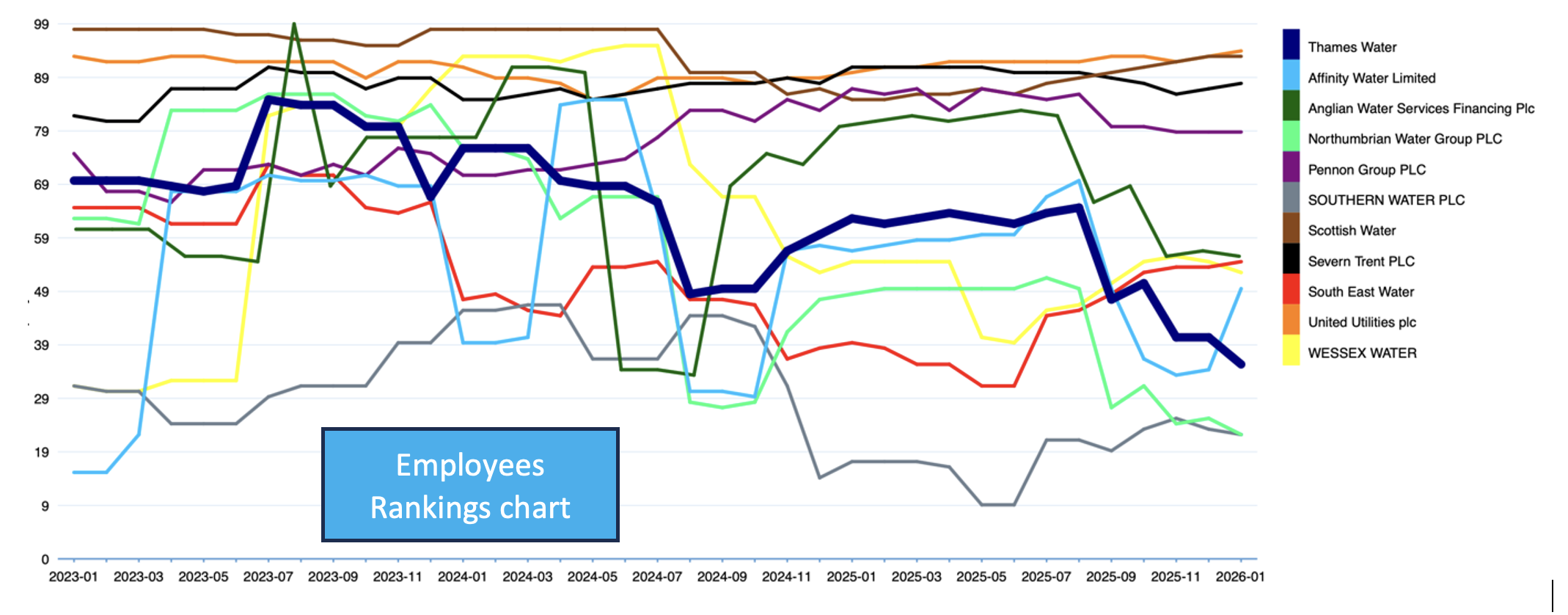

Inside the Organisation

The Employee Rankings show the shock did not remain external. After July 2024, Thames’s employee percentile fell from the high 60s into the mid-30s.

Workforce confidence reflects organisational stability. When governance weakens and scrutiny intensifies, internal perception follows.

In the drama, staff appear stretched and defensive. The data suggests internal sentiment shifted alongside public coverage.

The crisis became structural.

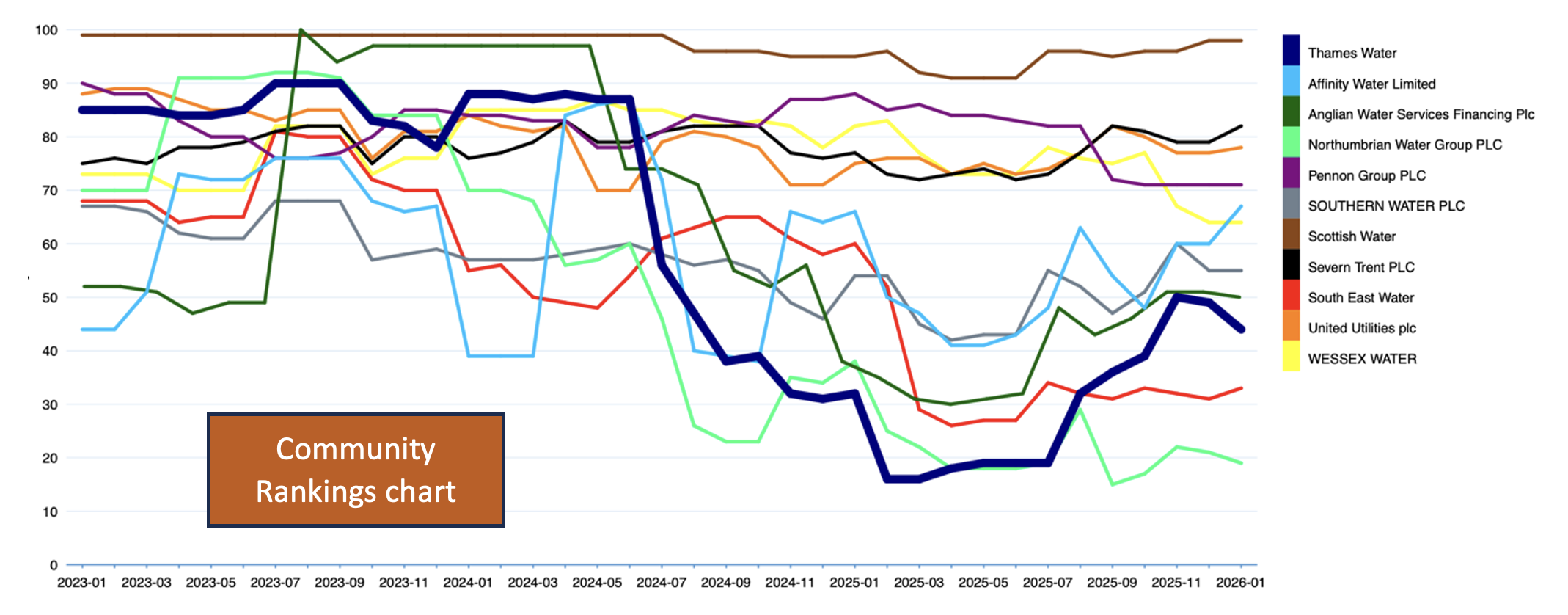

The Sharpest Drop: Community

Before mid-2024, Thames’s community percentile sat comfortably above 80. After the reporting wave and regulatory escalation, it collapsed into the teens by early 2025.

Community rankings capture stakeholder trust, NGO sentiment and visible public impact. They move faster than governance metrics because they respond directly to salience.

Once social licence weakens, it rarely rebounds quickly. In the programme, this is when the company realises it no longer controls the narrative. The data suggests that realisation occurred in late 2024.

The Overall Reset

Three years ago, Thames ranked in the mid-80s percentile among peers. By early 2026, it sits in the mid-40s.

Meanwhile: United Utilities plc, Severn Trent PLC, and Scottish Water remain consistently high.

The sector did not collapse. It diverged.

Not Just Thames Water

Thames is the most dramatic case — but not the only one. The charts show material relative declines for four other operators.

South East Water - Following major outage reporting in late 2025, South East trends downward in Overall and Employee rankings. Here the reputational trigger is resilience rather than sewage.

Southern Water - Long-running pollution scrutiny leaves Southern structurally weaker in Community and Overall dimensions. The decline is less abrupt but deeply embedded.

Northumbrian Water - Enforcement phases correspond with visible step-down patterns in rankings — a recalibration rather than collapse.

Wessex Water - Wastewater compliance attention through 2024–2025 coincides with drift from upper-tier positioning into mid-pack.

Different triggers. Same mechanism: visible operational or regulatory weakness followed by measurable relative downgrading.

What the Drama Understood

Dirty Business worked because it showed that institutional failure rarely arrives as a single rupture. It unfolds in sequence.

First, environmental performance is questioned.

Then governance structures come under scrutiny.

Internal confidence weakens.

External trust erodes.

Relative standing resets.

The programme dramatised that progression. The data traces it.

Across multiple ESG dimensions, the inflection appears in mid-2024. Environmental percentiles step down first. Governance follows. Employee and community sentiment deteriorate thereafter. The pattern is layered and directional.

This was not sector-wide collapse. Peer operators remained comparatively stable. What occurred was divergence — measurable, sustained, and company-specific.

The headlines amplified the story.

The data fixed the date.

Mid-2024 is where confidence bends.

From that point, the decline is not conjecture.

It is visible.